The Superannuated – A Ladder Strategy to Protect the Pension

Pension Protection

FDNY retirees generally can choose between two tools to protect (hedge) the value of their pensions:

1. Pension Beneficiary Option

2. Term Life Insurance

The beneficiary option is available to all retirees. The cost depends on the age of the pensioner and the age of the beneficiary. Life insurance is available to those that are healthy enough to qualify for it. Of the two choices, the beneficiary option tends to be more expensive than term life insurance. The beneficiary option also tends to cover the beneficiary for a longer period (end of their life) as opposed to term life insurance, which covers the beneficiary until the end of the term policy.

Retirement data shows that many retirees do not elect to take a beneficiary option. We believe that this result is driven by the cost effectiveness of term life insurance to protect the value of the pension. We assume (hope) that the retirees that do not select a beneficiary option are using insurance, and the right amount of insurance.

The Superannuated

In FDNY lingo the superannuated are those that are cordially shown the door at 65 years young. Many of these retirees have served for 35-40 years or more. In general, a longer service time (more time on the job) generates a higher pension. There is a cost to the higher pensions though. In general, as each year goes by both the potential pension beneficiary option and the potential term life insurance policy become more expensive. Usually, pensions of the superannuated are more expensive to protect relative to the pensions of those that retire younger.

In retirement, the superannuated should protect their pensions with a beneficiary option or life insurance, or a combination of the two. Retirees that are not healthy enough for life insurance will most likely select a beneficiary option. Retirees that are healthy enough for life insurance can choose between a beneficiary option or life insurance. One of the most common mistakes we see is retirees declining the beneficiary option and acquiring insurance, but not enough of it.

Understanding the value of the pension is key to making a sound decision between the beneficiary option and life insurance. The value of the pension is the beginning point to determine how much life insurance is required, before each retirees’ unique circumstances are considered. This will be illustrated in the case study below.

Pension Valuation

FDNY pensions are very similar to fixed income instruments. They are much more fixed income like than they are equity like. The pension pays fixed amounts at fixed time intervals, just like a bond or annuity does. Fixed income instruments can be valued with just a few inputs:

·Payment amount

Future value

Time

Interest rate (discount rate)

Sound easy? Not so fast. We know the first two inputs; payment amount is the annual pension amount and future value is zero since the pension eventually goes away. The time and interest rate variables are more challenging. We cannot know the time variable for sure, i.e., the length of the collection period, but we can make reasonable estimates like using average life expectancy. The appropriate discount rate is highly debatable. We prefer to use the current market rates on similar risk securities that trade in public markets. If the valuation is done properly a retiree should be indifferent to receiving the pension (fixed payments) or the estimated present value (lump sum) today.

In the case study below the estimated pension value will be key in the beneficiary vs. life insurance decision.

Case Study

Chief Davis

Staff Chief (DAC) Davis is being forced out after recently completing his 42nd year of service. He turns 65 next month and wants a plan of action by his birthday, i.e., the day he is superannuated. Chief Davis has always been a squared away fellow and he purchased a 30 year $1M term policy to protect his family when he was a new lieutenant 30 years ago. That policy is set to expire on his birthday in a few weeks and will no longer provide any protection. Chief Davis is willing to consider either the 100% pension beneficiary option, or a term life insurance policy. However, he does have a budget constraint. Chief Davis is not willing to spend more than $20,000 per year to protect his pension.

Pension Value

Chief Davis attends a retirement consultation and brings his numbers with him. After 42 years of service, he has earned an abnormally high service pension in the amount of $225,000 per year. Chief Davis will also receive the annual VSF (Variable Supplement Fund) payment of $12,000 per year and expects to pay an average tax rate of 22% in retirement. His wife Susan is several years younger than he is, and they expect to collect the pension for 20 years. Current market rates indicate an appropriate discount rate of 4.01% to value this pension. The Chief is surprised when the retirement advisor tells him that the value of his pension is estimated to be about $2.5M. However, the advisor reminds him that it took 42 years of service to build that pension value. The key details of the pension valuation follow:

Beneficiary Option and Life Insurance

Next, Chief Davis wants to compare the cost of the 100% beneficiary option to term life insurance. Chief Davis is surprised to learn that the cost of the beneficiary option is $28,000 per year. This is higher than his budget constraint of $20,000.

Armed with an estimated value of his pension and the cost of the beneficiary option, Chief Davis proceeds to a meeting with his insurance agent. Chief Davis had been considering $1M of term life but now realizes he was way off. His insurance agent agrees, and Chief Davis requests a quote for $2.5M (the pension value) for 20 years, providing coverage until he turns 85. The Agent tells Chief Davis that his requested policy would cost $22,000 per year. The insurance quote is lower cost than the beneficiary option but still over the budget of $20,000 per year. Chief Davis is growing frustrated but then he remembers that there is tremendous flexibility with the tools he has available to him. He requests that his advisor and insurance agent engineer a solution that covers his pension and meets his budget requirement.

The Ladder

Chief Davis briefly considers just buying less insurance to get him under the budget ceiling. His advisors tell him that less coverage won’t be sufficient to protect the pension. However, Chief Davis is excited to learn that they have engineered a potential solution well within his budget constraint. They suggest a laddered insurance solution with three different term life insurance policies:

A 10-year term of $1.5M for $6,300

A 15-year term of $500,000 for $2,800

A 20-year term of $500,000 for $4,400

The initial cost is $13,500 per year and initially provides $2.5M of term coverage. The Chief is ecstatic that he can protect the full value of his pension and be well within his budget constraint. The Advisors warn Chief Davis that this is not a “free o”, he is front loading the policy for cheaper premiums but accepting lower coverage in years 11-20. Total coverage and cost are as follows:

Years 1-10 have $2M of coverage and cost $13,500 per year.

Years 11-15 have $1M of coverage and cost $7,200 per year.

Years 16-20 have $500k of coverage and cost $4,400 per year.

Chief Davis understands that money has time value, so he is ok with front loading the ladder, but asks for more information. His Advisor provides him with the following summary table and informs him that 60% of the present value of his pension is captured in the first ten years (Total PV Capture Column):

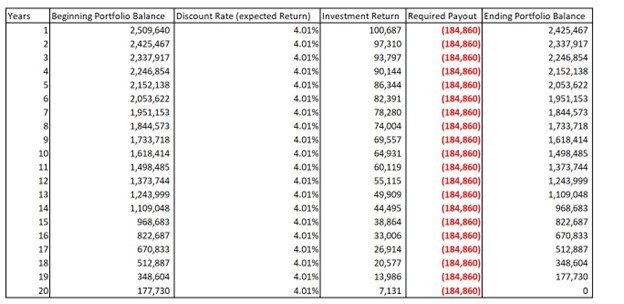

Chief Davis believes that if he collects the pension for 10 years he will add (save) enough money to his current investment portfolio that he will not require the full coverage amount beyond year 10. If he doesn’t collect the pension for at least 10 years his spouse will collect $2.5M of life insurance and his Advisor is confident that with the life insurance payout the investment portfolio can replicate the after-tax pension payments for twenty years. The Advisor provides Chief Davis with a table illustrating the pension replication if Chief Davis were to die the first day he was retired (and finalized). The beginning balance is the $2.5M life insurance payout plus $9,640 of cash in the Chiefs investment account.

Conclusion

FDNY retirees generally have two tools available to protect their pension, beneficiary options and life insurance. For the superannuated these tools are generally more expensive than they are for younger retirees, regardless of which tool is selected. The tools are also not perfect replacements for each other, but they do offer great flexibility. They can be used in isolation or in combination. Retirees that are not healthy enough for life insurance are guaranteed to be offered a pension beneficiary option. Retirees that are in great health may be able to get rates on an adequate amount of insurance that is far less expensive than a pension option. Regarding adequate life insurance, Brave Eagle Wealth Management considers the present value of the pension to be the starting point of the discussion to identify the amount needed. Done properly, this amount of life insurance, sometimes in combination with an investment portfolio, could be used to replicate pension payment amounts to the surviving spouse – or a different amount if the spouse doesn’t require the full pension amount.

In the case study above, we introduced an example of a real-world constraint specific to Chief Davis, in this case it was a budgetary constraint not to exceed $20,000 per year. Subject to that constraint, a term life insurance ladder strategy was designed to:

Initially protect the entire present value of the pension

Cost less than the maximum budget constraint of $20,000

In our hypothetical case study, the ladder strategy was acceptable to Chief Davis even though both the pension beneficiary option and the $2.5M 20-year term life insurance policy may have provided more protection. Each retiree’s personal situation is different and the optimal solution for each retiree can/will be different. This case study was intended as an example of one flexible solution among many.

Investment advisory services are offered through Brave Eagle Wealth Management, LLC; a New York domiciled registered investment advisor. All content is for information purposes only and should in no way be construed or interpreted as a solicitation to sell or offer to sell advisory services to any residents where it is not appropriately registered, excluded or exempted from registration or where otherwise legally permitted. It is also not intended to provide any tax or legal advice or provide the basis for any financial decisions. Nor is it intended to be a projection of current or future performance or indication of future results. Moreover, this material has been derived from sources believed to be reliable but is not guaranteed as to accuracy and completeness and does not purport to be a complete analysis of the materials discussed. Purchases are subject to suitability. This requires a review of an investor’s objective, risk tolerance, and time horizons. Investing always involves risk and possible loss of capital.